Choosing the right PPO (Preferred Provider Organization) provider is a pivotal decision that significantly impacts your healthcare experience. In the complex landscape of healthcare plans, selecting the one that aligns with your needs can be daunting. This comprehensive guide aims to simplify the process by highlighting key factors to consider when making this crucial choice.

How to choose a PPO network?

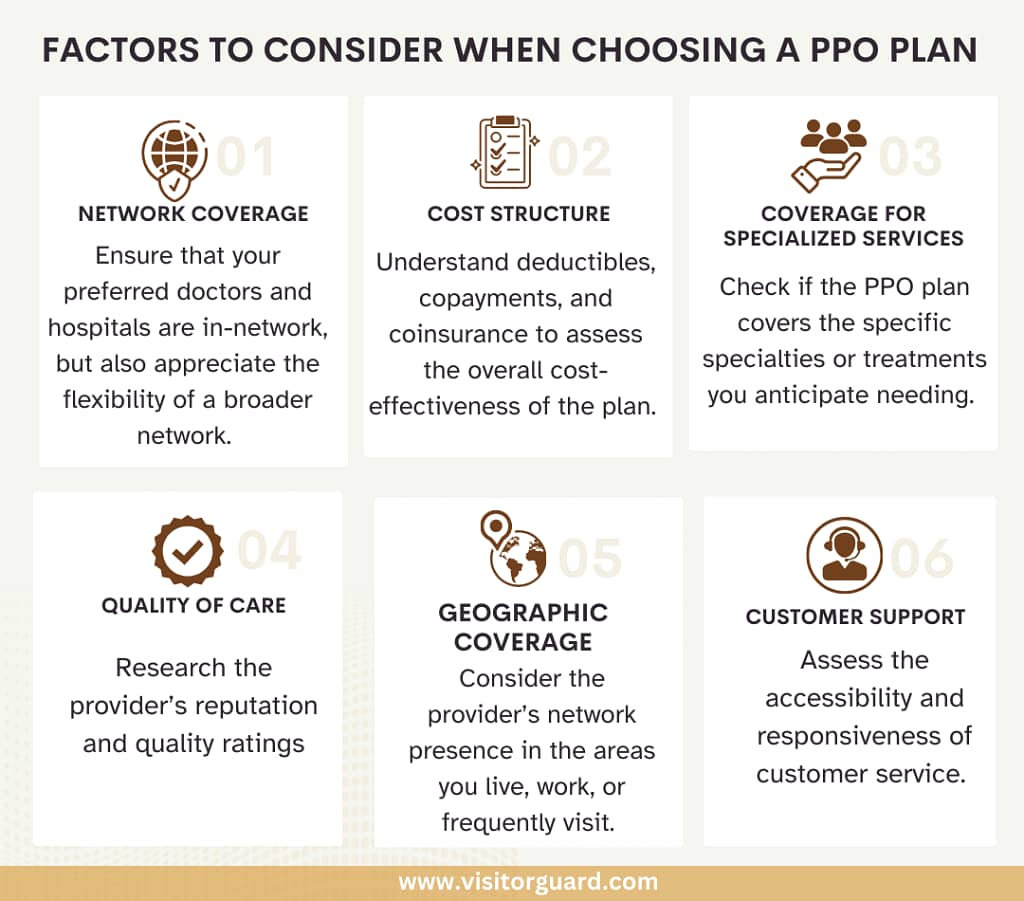

One of the fundamental aspects to assess when choosing a PPO provider is the extent of their network coverage. PPO network plans offer a unique advantage by allowing you to receive care from both in-network and out-of-network healthcare providers. Here is what you need to know:

In-network vs. Out-of-network: In-network providers have agreements with your insurance company, resulting in lower costs for you. It is crucial to check if your preferred doctors, specialists, and hospitals are in-network, as this can significantly affect your out-of-pocket expenses.

Preferred providers: PPO plans often have a list of preferred providers who offer services at reduced rates for plan members. These providers can be a cost-effective choice, and it is wise to consider them when seeking medical care.

Flexibility: PPO plans offer a broader network of healthcare providers. This extended network provides you with the flexibility to see specialists or receive treatment from out-of-network providers without needing a referral from your primary care physician.

How is cost determined in PPO networks?

Navigating the cost structure of a PPO plan is essential to manage your healthcare expenses effectively. Here is what you should consider:

Deductibles: Deductibles are the initial amount you must pay out of pocket before your insurance starts covering costs. Plans with higher deductibles often have lower monthly premiums, making them appealing to those who prefer to pay less each month but are willing to cover higher upfront costs when medical care is needed.

Copayments: Copayments are fixed amounts you pay for specific services, like doctor’s visits or prescription medications. PPO plans typically offer predictable copayment options, making it easier to budget for routine healthcare expenses.

Coinsurance: Some PPO plans use coinsurance, where you pay a percentage of the total cost of services. It is crucial to understand the coinsurance percentage and how it applies to various medical treatments. Plans with higher coinsurance may have lower monthly premiums but can result in higher out-of-pocket expenses.

Cost-sharing options: Compare the cost-sharing options of different PPO plans. Some may have higher deductibles but lower coinsurance, while others may offer lower deductibles but higher coinsurance.

Do PPO providers cover specialized services?

In-Network Specialists: PPO networks typically have a wide range of specialists within their network. If you need to see a specialist, it is advisable to choose one from the network. In-network specialists offer the advantage of lower out-of-pocket costs compared to out-of-network providers.

Out-of-Network Specialists: PPO plans provide some coverage for out-of-network specialists as well. However, you may have to pay a higher percentage of the costs when you choose an out-of-network specialist. Be sure to check your plan’s policy on out-of-network coverage for specialized services.

Referral Requirements: Many PPO plans do not require referrals to see specialists. This means you can schedule an appointment with a specialist directly without needing a referral from your primary care physician. This can be especially convenient when seeking specialized care.

Coverage for Specific Specialties: PPO plans usually cover a wide range of specialties, including cardiology, orthopedics, dermatology, oncology, and more. However, coverage may differ based on the plan. It is essential to review your plan’s benefits and network directory to confirm that the specific specialty you need is covered.

Prior Authorization: For certain specialized services or treatments, your PPO plan may require prior authorization. This means you must get approval from the insurance company before receiving specific treatments or services. Failing to obtain prior authorization could result in reduced coverage or denial of the claim.

By thoroughly assessing these aspects, you can tailor your choice to your unique healthcare requirements and preferences. Remember that there is no one-size-fits-all answer when it comes to PPO providers, so take your time, ask questions, and make a decision that prioritizes your health and well-being.

Pallavi Sadekar is a seasoned insurance professional with over 17 years of experience in the industry. As the Head of Operations at Visitor Guard®, she brings a wealth of expertise to the field. With a profound understanding of insurance, Pallavi has consistently demonstrated her commitment to helping clients make informed decisions about their coverage.

Pallavi’s insights and advice has earned her recognition in esteemed publications, including Forbes, USA Today, and various online platforms. Her contributions to these outlets have solidified her reputation as a trusted authority in the insurance domain. Whether it’s navigating the complexities of visitor insurance, finding the right coverage for clients, or understanding the intricacies of visitor health insurance, Pallavi’s in-depth knowledge allows her to offer practical and informed guidance to her clients.

For many travelers from India, visiting the United States, purchasing travel insurance is often seen as a mere formality. Many travelers choose the cheapest.

Chat With Us

Chat With Us